This morning, Kevin Warsh was sworn in as the 17th Chair of the Federal Reserve. If you don’t follow central bank appointments closely, you might be tempted to file this under “D.C. process news” and move on. Don’t. The person who chairs the Fed has more influence over your mortgage rate, your credit card APR, your savings yield, and the value of your investment portfolio than any elected official in the country. And what makes this transition particularly significant isn’t just who Warsh is — it’s when he’s arriving.

Who Is Kevin Warsh?

Warsh is 56 years old, a Stanford and Harvard Law graduate who spent his early career at Morgan Stanley doing M&A before joining the George W. Bush White House as a special assistant for economic policy. In 2006, Bush nominated him to the Federal Reserve Board of Governors, making Warsh — at 35 — the youngest person ever appointed to that role.

His timing was historically terrible, in the best possible way. Warsh served on the Board from 2006 to 2011, which means he was in the room for all of it: the collapse of Bear Stearns, the bankruptcy of Lehman Brothers, the AIG bailout, and the 2008 financial crisis response. As the Fed’s central liaison to financial markets during the crisis, he had a front-row seat to what happens when the system breaks.

He resigned in 2011, and the reason matters for understanding where he stands today. Warsh was skeptical — sometimes vocally — of the Fed’s aggressive post-crisis stimulus. He opposed the Fed’s decision to buy $600 billion in Treasury bonds (quantitative easing), arguing that large-scale asset purchases and near-zero benchmark interest rates risked distorting markets and undermining long-term price stability. In the years that followed, he became a prominent Fed critic from the right: too much intervention, too accommodative for too long.

That’s the person who just took the chair.

Why He Was Picked, and Why That’s Complicated

President Trump nominated Warsh in January 2026, and the Senate confirmed him 55-45 on May 13 — with all Republicans and one Democrat (Sen. John Fetterman of Pennsylvania) voting in favor.

The political logic was transparent: Trump wanted lower interest rates. He’s said so repeatedly and publicly. And Warsh had offered a theory for why the Fed could cut rates aggressively without stoking inflation — centered on AI-driven productivity gains. The argument goes that as artificial intelligence accelerates output across the economy, supply expands fast enough to offset demand-side price pressures, giving the Fed room to run looser monetary policy.

It’s a legitimate thesis. Some credible economists hold versions of it. But here’s the problem: that thesis was developed before Iran.

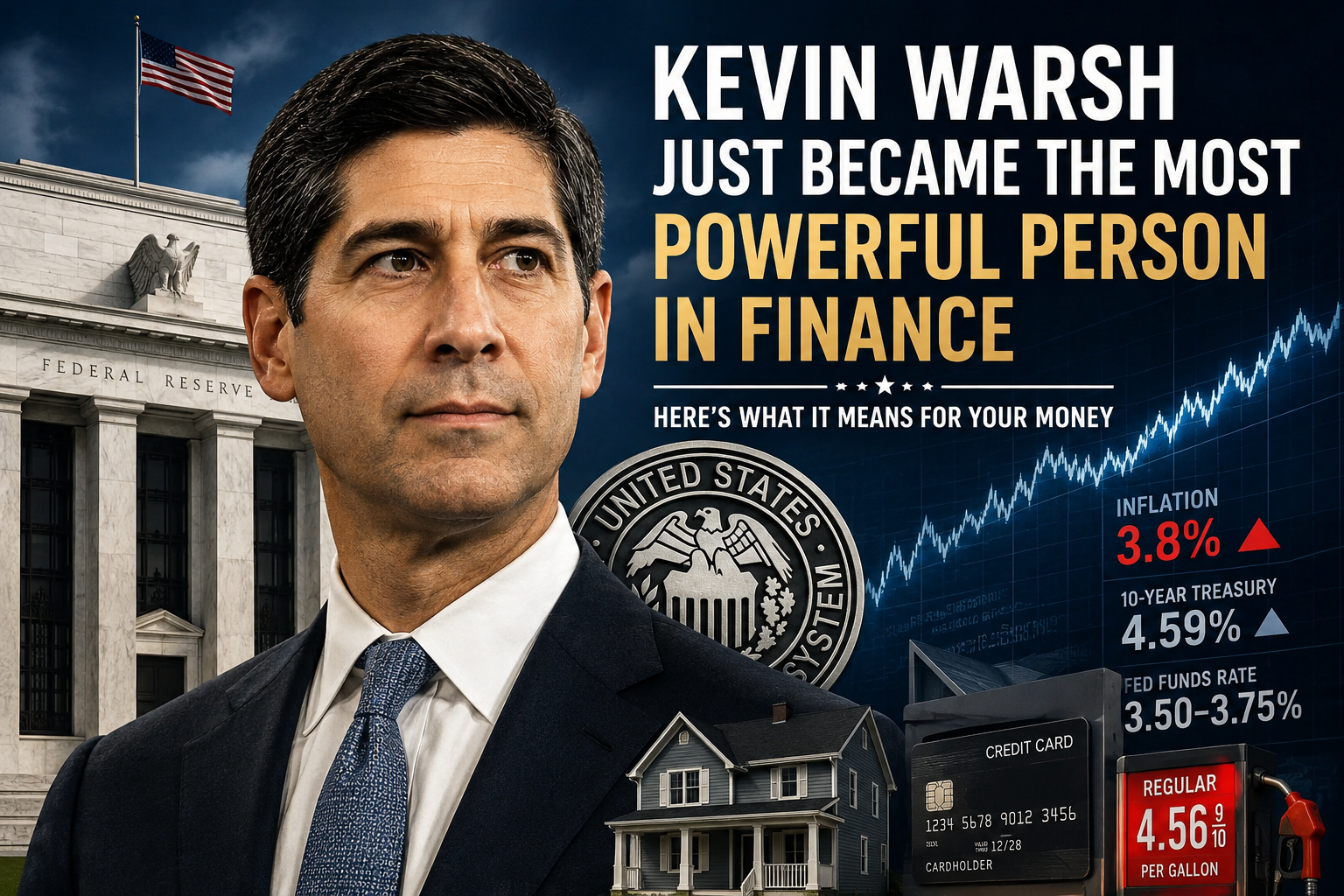

The bombing of Iran in late February 2026 sent crude oil surging, disrupted global supply chains, and kicked inflation higher across essentially every category of goods and services. The April Consumer Price Index came in at 3.8% year-over-year — the hottest reading since May 2023, and nearly double the Fed’s 2% target. Airfares are up 20.7% year-over-year. Gas is at $4.56 a gallon, a four-year high. The AI productivity disinflation thesis is hard to square with a world where every U.S. state has average gas prices above $4.

The Federal Open Market Committee (FOMC) — the group of Fed officials who actually vote on interest rates — has been in no mood to cut. And according to reporting from CNBC, Warsh walks into a “big family fight” within the Fed over the rate path. The FOMC tends to move by consensus, and several current members are focused on getting inflation back to 2% before loosening policy, not on productivity theories.

What’s Likely to Happen With Rates

Jerome Powell’s final act as chair held the benchmark fed funds rate at 3.50–3.75%. The next scheduled FOMC meeting is June 16-17 — Warsh’s first as chair.

The honest answer is that nobody knows exactly what he’ll do. But here’s what we can reason through:

Warsh cannot cut rates with CPI at 3.8% without serious political and credibility risk. The Fed’s entire institutional mandate rests on controlling inflation. Cutting into a 3.8% print, with oil above $100 and consumer inflation expectations rising (the University of Michigan survey has year-ahead expectations at 4.5%), would be the kind of move that undermines central bank credibility for years.

At the same time, Atlanta Fed’s GDPNow tool currently tracks Q2 GDP growth at roughly 4%, and unemployment sits at 4.3%. The economy is not in recession. There’s no growth emergency that demands immediate rate cuts.

The most likely near-term outcome: rates hold at 3.50–3.75% at the June meeting while Warsh assesses the data and begins shaping the FOMC’s direction. If inflation proves stubborn through the summer — which is plausible given ongoing oil price pressure — there is a real scenario where rates rise under Warsh before they fall. That would be a significant shift from market expectations at the start of the year, when many investors were pricing in two or three cuts by year-end.

What This Means for Your Finances

If you’re wondering how any of this connects to your actual life, here are the transmission mechanisms that matter most.

Mortgages: The 30-year fixed mortgage rate tracks the 10-year Treasury yield more than the fed funds rate directly. The 10-year ended this week at 4.59%, the highest in over a year. If Warsh signals hawkishness or the market prices in a rate hike, that yield climbs further and so does the cost of buying a home. For a $400,000 mortgage, the difference between a 6.5% and 7.0% rate is about $130/month — roughly $1,560/year.

Credit cards: Variable-rate credit cards are directly tied to the prime rate, which moves with the fed funds rate. If rates hold or rise, that 21–24% APR on your revolving balance stays exactly where it is or goes higher. This is the most direct and painful channel for anyone carrying a balance month-to-month.

Savings accounts and CDs: High-yield savings accounts and certificates of deposit have been paying meaningful rates for the first time in years — and that continues if rates stay elevated. If you haven’t moved idle cash from a legacy 0.01% bank account into a high-yield account, you’re leaving real money on the table.

Equities: Rate uncertainty is already showing up in markets. The 10-year yield moved roughly 60 basis points higher over the last three months, and that’s been a headwind for stocks even as corporate earnings — including Nvidia’s historic $81.6B quarter this week — have come in strong. If Warsh signals tighter policy, expect equity volatility to pick up, particularly in rate-sensitive sectors like real estate, utilities, and high-growth tech.

Crypto: Rising rates and a strong dollar environment historically pressure risk assets including Bitcoin, which has been struggling to break above its 200-day moving average near $82,000. If the rate trajectory shifts hawkish under Warsh, that’s an additional headwind for the crypto recovery thesis.

The Bottom Line

Kevin Warsh is a smart, experienced person who has spent decades thinking about monetary policy and market dynamics. He’s not a political puppet, and the Federal Reserve’s institutional independence — while perpetually debated — remains structurally intact. He will face real pressure to cut rates from the administration that appointed him, real pressure to hold or hike from FOMC colleagues watching inflation data, and real pressure from markets that have baked in certain assumptions about the rate path.

His first substantive remarks in the new role will be the most closely watched Fed communication in years. Watch for any speech, press conference, or Congressional testimony in the next few weeks. The words he chooses about “temporary” vs. “persistent” inflation — and whether he echoes or distances himself from the AI productivity thesis — will tell the market more about the next 18 months of monetary policy than anything else he could do on Day 1.

The most powerful person in finance just clocked in for his first day of work. It’s worth paying attention.

Sources: Kevin Warsh Confirmed as Fed Chair — NPR | Kevin Warsh Wins Senate Confirmation — CNBC | Warsh Faces ‘Family Fight’ Over Rates — CNBC | Warsh Sworn In, Inflation Complicates Path — Yahoo Finance | Kevin Warsh Could Prove Independent — The Conversation | Schwab Market Update May 21 | Warsh to Be Sworn In May 22 — Consumer Finance Monitor